Table of Content

FHA lenders must look at the borrower’s income stability and employment history for the past two years. Job-hoppers and borrowers with gaps in their job history may have to provide extra documentation and explanations to be approved. You’ll need at least a 3% down payment for a conventional loan. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appears on this site . LendingTree does not include all lenders, savings products, or loan options available in the marketplace. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site .

This requirement means Home Possible cannot be used for vacation homes or investment properties where the borrower does not live on-site. Home Possible requires a minimum credit score of 660 for all borrowers. These score requirements are higher than other programs like FHA or Fannie Mae’s HomeReady program .

Get Daily Mortgage Rate Updates & News

This makes it much easier for a large number of people to secure financing for a home than ever before. Applicant subject to credit and underwriting approval. Receipt of application does not represent an approval for financing or interest rate guarantee. Guaranteed Rate, Inc. does not guarantee the quality, accuracy, completeness or timelines of the information in this publication. While efforts are made to verify the information provided, the information should not be assumed to be error free. Some information in the publication may have been provided by third parties and has not necessarily been verified by Guaranteed Rate, Inc.

USDA loans don’t typically require cash reserves unless you’re applying for an exception for a high DTI ratio. Your total household income is counted, including non-borrowers. All family member incomes must be included in the calculations to make sure the total income is at or below your neighborhood income limits. VA-approved lenders must order appraisals through the VA’s online system. The VA appraisal can only be completed by a VA-approved appraiser to verify the property meets minimum VA property standards.

Home Possible Income Limits

That’s why your yearly income cannot exceed this threshold,” Francies notes. “This program is intended to help people whose income is 80% or less of the area median income by providing low down payment options and flexible sources of down payment funds,” Maxwell says. For most of the United States, the maximum conforming loan limit for one-unit properties will be $726,200 in 2023, up from $647,200 in 2022. For areas with higher-than-average home values, defined as places where median home values exceed 115% of the baseline, the FHFA has set a limit of $1,089,300 for 2023, up from $970,800 in 2022. And loans like the Freddie Mac Home Possible® mortgage, which are designed specifically to help low- and moderate-income borrowers buy a home, give you flexibility in how you reach that 3% threshold.

One big advantage of conventional loans over government-backed loan programs is that borrowers can purchase a second home or rental property. Government-backed loan programs only allow you to finance a primary residence you live in full time. The minimum credit score under the Home Possible program varies by lender, just like any other conventional loan.

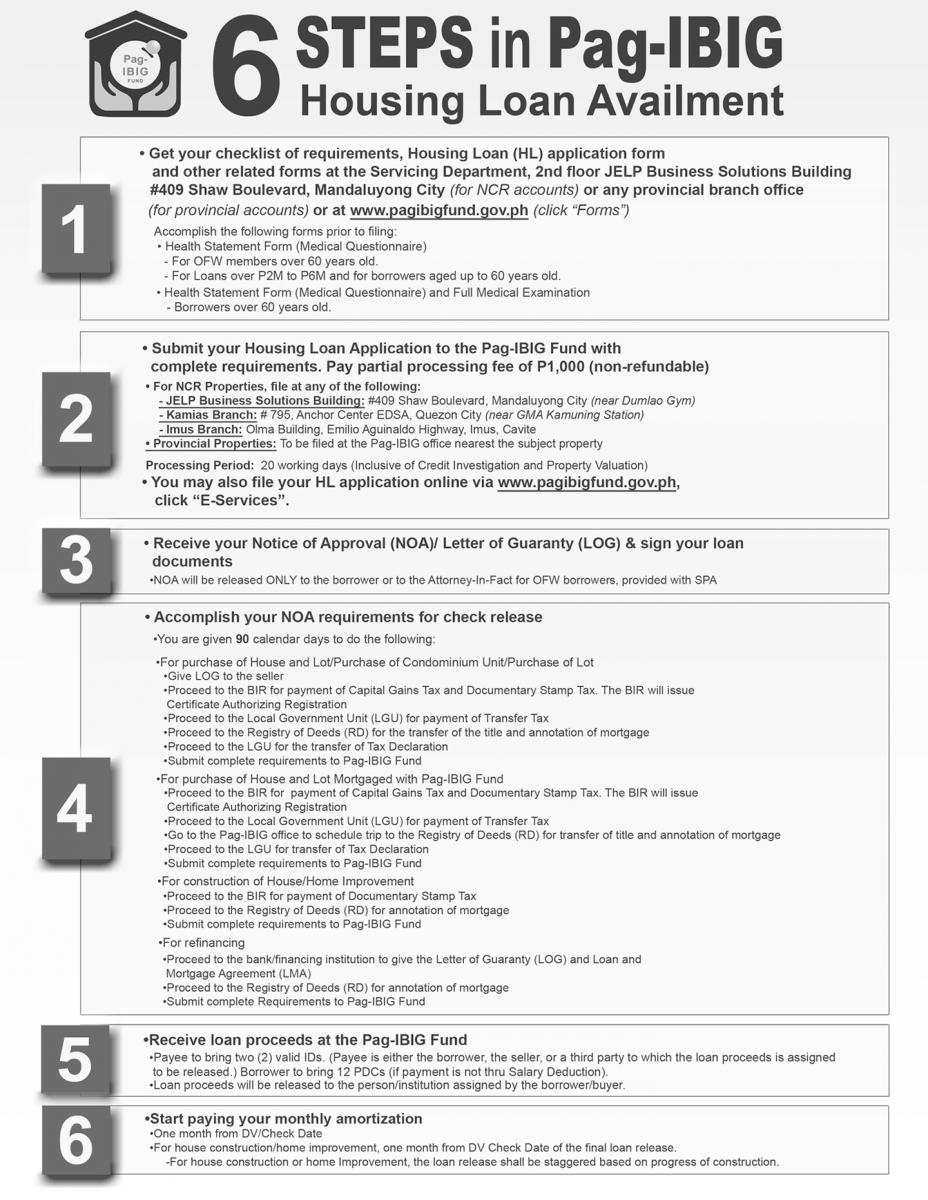

Common Mortgage Requirements for First-Time Home Buyers

Lenders require proof of steady income and need to verify the income is likely to be predictable in the future. You’ll typically need to document two or more years of variable income earned from commissions, bonuses or overtime. Borrowers must put down at least 5% when using the Home Possible program. The good news, however, is that the money does not have to be your own. You can use funds from family, friends, or an employer.

Conventional loan guidelines typically require a home appraisal, which is an unbiased opinion of a home’s value from a licensed property appraiser. Borrowers making at least a 20% down payment on a one-unit home may be eligible for a property inspection waiver and can skip a home appraisal. Conventional loans, which remain the most popular mortgage option, aren’t guaranteed by any government agency. Instead, lenders that offer conventional home loans follow rules set by government-sponsored enterprises Fannie Mae and Freddie Mac, which tend to be more stringent than government-backed mortgages. One unique aspect of the Home Possible program is the amount of income that is allowed. Because the program is for low to moderate-income families, you can only make a certain amount of money in order to qualify for the loan.

However, you may be able to use other forms of down payment assistance. Fannie Mae and Freddie Mac were chartered separately by Congress in 1938 and 1970 before being spun off into shareholder-controlled companies. Currently, they’re government-sponsored entities under the Federal Housing Finance Agency. Although founded at different times, they have a shared mission of providing mortgage funds that are affordable for the general public. According to Freddie Mac’s requirements, you’ll need a FICO score of 660 or higher to qualify for a Home Possible loan. Planet Home Lending is an approved Freddie Mac Home Possible® lender.

They consider income as part of your debt-to-income ratio. This is the percentage of your gross monthly income — your pre-tax income before deductions — that goes toward minimum debt payments. Your DTI ratio tells lenders the monthly mortgage payment you can afford. If you are a borrower, consult with your lender to make sure you fulfill your homebuyer education requirements with an approved program. Lenders, make sure you understand your investors’ homebuyer education requirements. Do all Home Possible borrowers need to take a homeownership education course?

Freddie Mac Home Possible is a conventional loan designed to help low- to moderate-income borrowers buy a home with 3% down. Down payment and closing cost assistance programs can also help lower the upfront costs of buying a home. These programs vary by location, so check with your state housing agency to see what you might be eligible for.

The Home Possible Program offers a lower down payment than FHA loans. Home Possible loans require only 3% down (compared to the FHA minimum of 3.5%) and offer several options for gathering down payment funds without digging into your own pocket. The Home Possible Program is a mortgage program sponsored by Freddie Mac to make homeownership more attainable for first-time and low to middle-income borrowers. Median home values generally increased in high-cost areas in 2022, which increased their conforming loan limits . The new ceiling loan limit for one-unit properties will be $1,089,300, which is 150 percent of $726,200, FHFA said in its announcement.

As a self-employed borrower, be mindful that too many business deductions on your tax return can reduce your qualifying amount. Lenders use your net income after deductions for qualifying purposes. They can add back some deductions, such as those for mileage and use of a home office. As a rule of thumb, the more business deductions you have, the less you earn on paper. In general, you can’t make more than 100% of the average median income for the area. This is the case unless you live in a low-income census tract.

A score of 580 is required for borrowers making a minimum down payment of 3.5%. FHA-approved lenders also use the Credit Alert Verification Reporting System, or CAIVRs for short, to confirm you don’t have any delinquent federal debt like student loans. It may be easier to qualify for a mortgage backed by the Federal Housing Administration than a conventional loan. FHA-approved lenders are protected against losses when you pay for FHA mortgage insurance. This extra insurance allows lenders to make loans to borrowers with lower credit scores and more debt than conventional loans, because their losses are paid by the insurance if the borrower defaults.

Other requirements to qualify for a mortgage

The results show you would need to have an income below $64,640/year to qualify for the Home Possible program. Coming up with enough money for a down payment can be difficult. The Federal Home Loan Mortgage Corporation, also known as “Freddie Mac,” oversees the Home Possible program. Read on to learn more about how these programs could help you buy a home. Mortgage.info is your information portal for all things home, mortgage, and refinancing. You’ll need to document at least two years of self-employment for an FHA loan.

No comments:

Post a Comment